Latest Updates

- President Trump signed the One Big Beautiful Bill Act into law on July 4, 2025.

- This update adds refined modeling results reflecting the amendments made in the Senate to the final version of the One Big Beautiful Bill Act, now passed by both chambers of Congress to be signed by the president.

- The One Big Beautiful Bill Act was amended before being passed out of the Senate.

The Good, the Bad, and the Ugly in the One Big Beautiful Bill Act

The One Big Beautiful Bill Act makes many of the individual tax cuts and reforms of the TCJA permanent. It improves upon the TCJA by making expensing for R&D and equipment permanent. However, for the most part, it does not include further structural reforms, and instead introduces many new, narrow tax breaks to the code, adding complexity and raising revenue costs.

7 min read

“One Big Beautiful Bill Act” Tax Policies: Details and Analysis

We estimate the One Big Beautiful Bill Act would increase long-run GDP by 1.2 percent and reduce federal tax revenue by $5 trillion over the next decade on a conventional basis.

11 min read

The One Big Beautiful Tax Bill: What’s In It, What’s Out

Congress is racing to pass the One Big Beautiful Tax Bill before the July 4 deadline. In this episode, Kyle Hulehan and Erica York break down what just happened over the weekend, what’s actually in the bill, and what comes next as the House and Senate try to reconcile their differences.

The Senate Finance Committee’s New International Tax Package: A First Look

The Senate draft overall makes more changes to international tax policy than the House draft. On net the changes are positive.

8 min read

Senate Softens Blow for Pass-Throughs Using Current SALT Workarounds

The Senate’s version of the OBBB restores the benefit of avoiding the SALT deduction cap with PTETs for all pass-through businesses, while placing new limits on the extent of the workarounds.

6 min read

Breaking Down the Senior Deduction in the One, Big, Beautiful Bill

The House-passed reconciliation bill leaves out Trump’s promise to eliminate taxes on Social Security benefits, opting instead to expand the standard deduction for seniors.

“One Big Beautiful Bill Act” House GOP Tax Plan: Details and Analysis

Our preliminary analysis finds the tax provisions increase long-run GDP by 0.8 percent and reduce federal tax revenue by $4.0 trillion from 2025 through 2034 on a conventional basis before added interest costs.

9 min readTrump Tariffs: Tracking the Economic Impact of the Trump Trade War

The tariffs amount to an average tax increase of nearly $1,200 per US household in 2025.

39 min read

A More Generous SALT Deduction Cap in the Big, Beautiful Bill Would Cost Revenue and Primarily Benefit High Earners

Letting the SALT cap slip further upwards would undercut the TCJA’s long-term legacy, worsening the fiscal outlook of the tax package and providing an unneeded benefit to higher earners.

4 min read

Current Trump Tariffs Threaten to Offset Benefits of Promised Tax Cuts

While Congress works on the “One, Big, Beautiful Bill” to cut taxes, President Trump has imposed significantly higher taxes by placing tariffs on more than 70 percent of US imports.

2 min read

The One Big Beautiful Bill, Explained

We break down the House GOP’s One, Big, Beautiful Bill—a sweeping tax package designed to extend key parts of the 2017 Tax Cuts and Jobs Act before they expire in 2026.

Three Corporate Tax Hikes That Would Undermine TCJA’s Improvements to Competitiveness

As lawmakers consider options for budgetary offsets, they should prioritize competitiveness and economic growth, as a heavier corporate tax burden will undermine the core purpose and achievement of the TCJA.

24 min read

House Tax Package Could Double Economic Growth Impact by Prioritizing Permanence for TCJA Business Provisions

As the current tax package stands, the House’s use of temporary policy is leaving most of the economic growth opportunities on the table.

2 min read

House “One Big Beautiful Bill” Riddled with Temporary Tax Policy

As lawmakers continue to debate the “One Big Beautiful Bill,” they should abandon temporary and complex policy in favor of simplicity and stability.

4 min read

House GOP’s Approach to the IRA Clean Energy Tax Credits: Five Things to Know

Tax simplification has two aspects. The first is a code without a mess of targeted provisions for various social policy goals. The second is a code with provisions that are simple and easy to comply with. The bill succeeds at the first, but fails at the second.

7 min read

Growth Should Be a Key Consideration if Corporate SALT Is Limited

Lawmakers should prioritize pro-growth tax policies and use the least economically damaging offsets to make the legislation fiscally responsible. If lawmakers choose to use C-SALT, they should carefully consider the economic trade-off with permanent, pro-growth tax cuts that support investment and innovation in the US.

7 min read

Overview of the Tax Foundation’s General Equilibrium Model

The Tax Foundation uses and maintains a General Equilibrium Model, known as our Taxes and Growth (TAG) Model to simulate the effects of government tax and spending policies on the economy and on government revenues and budgets.

9 min read

Making the Tax Cuts and Jobs Act Permanent: Economic, Revenue, and Distributional Effects

Permanently extending the Tax Cuts and Jobs Act would boost long-run economic output by 1.1 percent, the capital stock by 0.7 percent, wages by 0.5 percent, and hours worked by 847,000 full-time equivalent jobs.

6 min read

New Directions in Tax Policy: Budgetary and Other Challenges of an Increasingly Complex Tax Code

The Tax Foundation, University of North Carolina Tax Center, and Massachusetts Institute of Technology Sloan School of Management are hosting a joint conference to discuss New Directions in Tax Policy: Budgetary and Other Challenges of an Increasingly Complex Tax Code.

Options for Navigating the 2025 Tax Cuts and Jobs Act Expirations

Policymakers should have two priorities in the upcoming economic policy debates: a larger economy and fiscal responsibility. Principled, pro-growth tax policy can help accomplish both.

21 min read

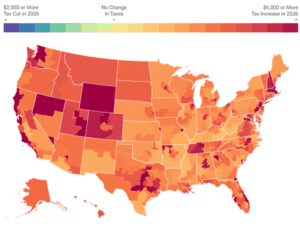

Expiring TCJA Tax Provisions in 2026 Would Produce Substantial Tax Hike across the US

At the end of 2025, the individual tax provisions in the Tax Cuts and Jobs Act (TCJA) expire all at once. Without congressional action, most taxpayers will see a notable tax increase relative to current policy in 2026.

4 min read

Tax Calculator: How the TCJA’s Expiration Will Affect You

Unless Congress acts, Americans are in for a tax hike in 2026.

3 min read

A Tax Reform Plan for Growth and Opportunity: Details & Analysis

This tax reform plan would boost long-run GDP by 2.5%, grow wages by 1.4%, and add 1.3M jobs, all while collecting a similar amount of tax revenue as the current code and reducing the long-run debt burden.

38 min read-

Erica York is Vice President of Federal Tax Policy with Tax Foundation’s Center for Federal Tax Policy. Her analysis has been featured in The Wall Street Journal, The Washington Post, Politico, and other national and international media outlets.

-

Garrett Watson is Director of Policy Analysis at the Tax Foundation, where he conducts research on federal and state tax policy. His work has been featured in The Washington Post, The Atlantic, Politico, the Associated Press and other major outlets.

-

Alex Muresianu is a Senior Policy Analyst at the Tax Foundation, focused on federal tax policy. Previously working on the federal team as an intern in the summer of 2018 and as a research assistant in summer 2020. He attended Tufts University, graduating with a degree in economics and minors in finance and political science.

-

Dr. William McBride is the Chief Economist & Stephen J. Entin Fellow in Economics at the Tax Foundation, where he oversees major research projects primarily related to reforming the federal tax code, advancing sound tax policy, and improving the federal government’s fiscal outlook.