North Dakota‘s tax system ranks 9th overall on the 2025 State Tax Competitiveness Index. North Dakota performs above average across all tax categories, ranking in the top 10 states overall, as well as on the property tax and corporate tax components. While North Dakota’s corporate and individual income taxes have a graduated-rate structure, both rates are low, with North Dakota’s top marginal individual income tax rate tied with Arizona’s as the lowest in the country (2.5 percent).

One shortcoming in North Dakota’s tax code is its throwback rule, which increases tax liability for in-state businesses making sales of tangible personal property in states with which they lack nexus.

However, North Dakota conforms to federal expensing provisions under Section 168(k) and 179, conforms to the federal treatment of NOLs, and does not levy a capital stock tax, real estate transfer tax, or estate or inheritance tax.

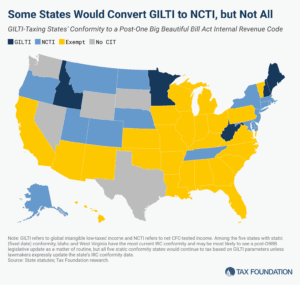

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).