Michigan‘s tax system ranks 14th overall on the 2025 State Tax Competitiveness Index. Michigan’s tax code includes all major tax types and has traditionally ranked well on the Index. The state’s individual income tax is flat with a relatively low rate of 4.25 percent (temporarily reduced to 4.05 percent in 2023), along with a modest personal exemption. However, Michigan faces significant regional competition, as Indiana, Ohio, and Pennsylvania all have lower state individual income tax rates, although all four states authorize localities to impose local income taxes.

Michigan has a flat 6 percent corporate income tax, which is higher than the national average. Unlike Ohio, the state does not impose a gross receipts tax and has no throwback rule or capital stock tax. However, the state does not offer full expensing, which could be an important element of future pro-growth reforms aimed at attracting capital-intensive businesses.

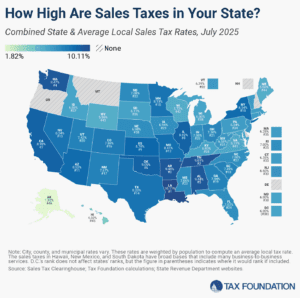

The state’s sales tax rate is 6 percent, lower than in all other Midwestern states except Wisconsin. Michigan does not authorize cities and counties to impose local option sales taxes, simplifying the consumption tax system compared to most other states.

Michigan’s property tax system is reasonably competitive with an average property tax burden. The state taxes tangible personal property but offers a generous de minimis exemption of $180,000, reducing compliance costs for small businesses. Michigan also does not impose estate, inheritance, or gift taxes, making it more attractive for high-net-worth individuals.

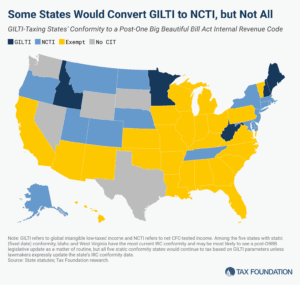

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

If Michiganders are interested in increasing the state’s spending on education or other priorities—and believe that current revenues are insufficient to support such an increase—there are several ways to do so without significantly affecting residents’ incentives to live and work in Michigan.