Arkansas‘s tax system ranks 36th overall on the 2025 State Tax Competitiveness Index. Arkansas ranks poorly on the Index despite multiple rounds of income tax rate reductions since 2015 and a resulting low top marginal individual income tax rate, due to a range of structural shortcomings in the state’s tax code. For instance, Arkansas only allows corporations’ net operating losses (NOLs) to be carried forward for 8 years, while most states either allow 20-year or uncapped carryforward periods. The state stands alone in having two different income tax rate schedules depending on taxpayer income.

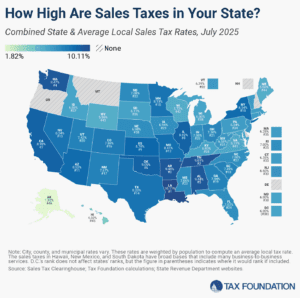

Arkansas also has the third-highest combined state and local sales tax rate in the nation at 9.46 percent. The state also imposes a tax on capital stock, at 0.3 percent of the apportioned net worth of corporations. Such taxes are increasingly rare, and Arkansas’s tax rate is the highest in the nation. The state also assesses property tax on businesses’ inventory, making the state even more of an outlier. Both taxes are assessed whether the firm makes a profit or loss in a particular tax year, which is harmful to small businesses seeking to scale up their operations, capital-intensive firms, and all firms during an economic decline.

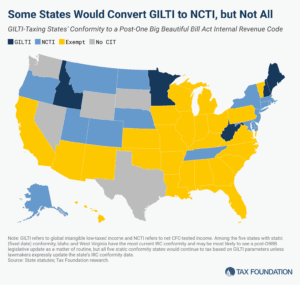

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).